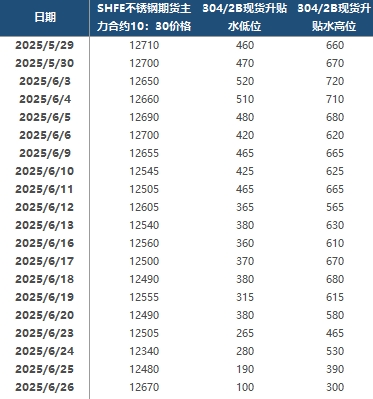

SMM reported on June 26 that the SS futures market continued to maintain a strong upward trend, driven by the general rise in non-ferrous metal futures and news of production cuts by steel mills, successfully breaking through the 12,600 yuan/mt threshold. In the spot market, steel mills' morning pricing continued to climb, and market quotes also strengthened. Although the overall increase was not as rapid as that in the futures market, low-priced supplies had largely disappeared. Against the backdrop of prices halting their decline and rebounding, despite a strong wait-and-see sentiment prevailing in the market, there were clear signs of a recovery in market transactions compared to the previous period. With transactions warming up this week, stainless steel social inventory declined, falling below 1 million mt again. Additionally, when steel mills' pricing was at a low level earlier, traders were more willing to purchase futures orders, thereby alleviating steel mills' shipping pressure to a certain extent.

In the futures market, the most-traded SS2508 contract strengthened and rose. At 10:30 a.m., SS2508 was quoted at 12,670 yuan/mt, up 19 yuan/mt from the previous trading day. In the Wuxi region, the spot premiums/discounts for 304/2B stainless steel ranged from 100-300 yuan/mt. In the spot market, cold-rolled 201/2B coils in Wuxi and Foshan were both quoted at 7,625 yuan/mt; cold-rolled trimmed 304/2B coils had an average price of 12,700 yuan/mt in Wuxi and the same in Foshan; cold-rolled 316L/2B coils were priced at 23,800 yuan/mt in Wuxi and the same in Foshan; hot-rolled 316L/NO.1 coils were quoted at 23,100 yuan/mt in both regions; cold-rolled 430/2B coils were both priced at 7,350 yuan/mt in Wuxi and Foshan

. Currently, the stainless steel market is still in the traditional off-season for consumption, with downstream demand failing to match the current supply level. Additionally, uncertainties such as US tariffs remain significant, leading to a strong wait-and-see sentiment among downstream players. Despite stainless steel mills generally facing losses and news of production cuts emerging in the market, due to the large base of previous production, current market supply remains at a historically high level for the same period, and the restoration of the supply-demand relationship will take time. Both steel mill inventory and social inventory are at relatively high levels. Against the backdrop of the off-season for consumption, the de-stocking speed has slowed down significantly, putting significant shipping pressure on stainless steel mills, agents, and traders, thereby limiting the rebound in stainless steel prices. The raw material side is also under tremendous pressure. Affected by expectations for production cuts by steel mills, only high-carbon ferrochrome has managed to maintain stable steel bidding prices amid production cuts by overseas ferrochrome producers, but market retail prices have already fallen below steel bidding prices. The prices of other raw materials, such as high-grade NPI and stainless steel scrap, have also weakened significantly, further eroding the cost support for stainless steel. The market is now waiting to see how the supply-demand relationship will recover after stainless steel mills implement production cuts.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)